Better Virtual Reality through Fantasy

Apple, Meta, and Finding the Product-Market Fit for VR Experiences

We’re in the wrap up for a significant year in technology and gaming. I’ll save words reviewing this past year, and looking forward towards the new one, for January when I’ll also be off to CES to discuss the newest buzzy tech (AI) as it pertains to gaming. We’ll instead end the year with an overview of a notable advancement in one of the other buzzy technologies in gaming, because for all the bluster and trend-chasing around AI we may have missed the fact that something actually transformative happened in the VR space over the past few months.

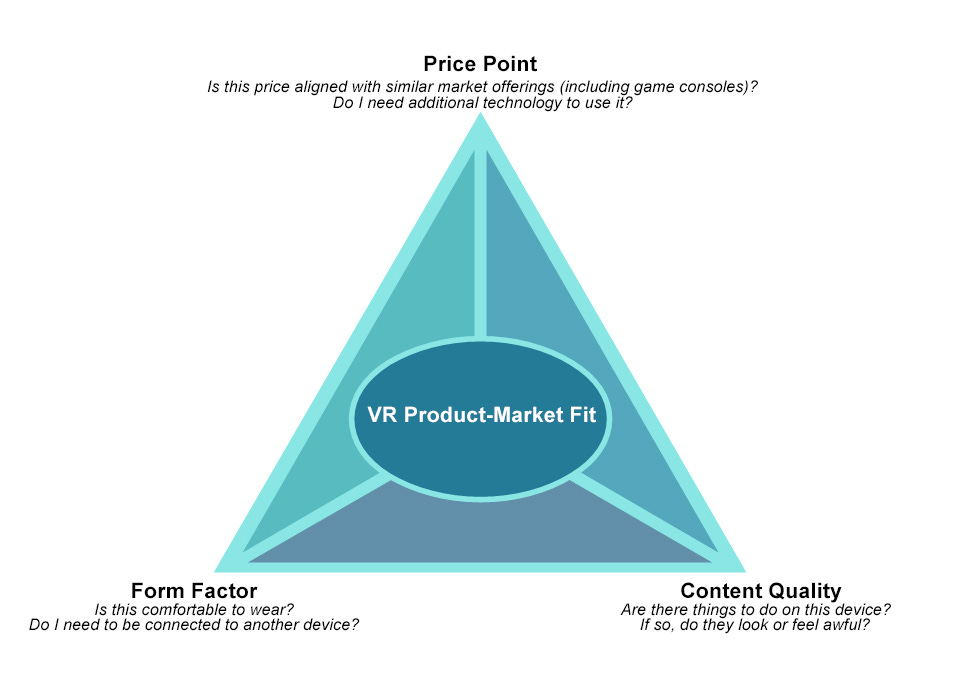

I’d never go so far as to say I’m a VR cynic, but I am a VR realist. And the reality of VR (for gaming applications or otherwise) has hardly been a slam dunk. VR has a steep hill to climb - mass adoption means offsetting the negatives of the tech relative to upside, and the negatives have historically far outweighed the core experiences (i.e. what we are left with once we pass the novelty factor). In general, VR technology has been expensive, cumbersome, and only offered a handful of experiences that often ended up being kind of ugly (due to either limited processing power or screen fidelity that wasn’t quite up to the job of being only a few millimeters from the eye). Triangulating an attractive consumer proposition in balance of this “trinity of VR product-market fit considerations” (price point, form factor, and content quality) has been the ongoing blocker for VR technology.

All that being said, I think we are finally getting close to a good balance in the final few months of this year. And no, I don’t think it has much to do with Apple (more on that momentarily).

It’s fashionable to hate on Meta, particularly as it pertains to the pivot into their new namesake, but I’d argue they’ve done more for the commercial adoption of VR (and to the extent you believe that it is both feasible and contingent upon VR technology, the Metaverse) than just about any technology company. The Q4 release of the Meta Quest 3 (MQ3) strikes an attractive balance in the aforementioned trinity - it’s reasonably affordable (roughly comparable with a gaming console), has a decent formfactor that doesn’t require external wires and allows for a quick “reality check” via vastly improved passthrough tech (thereby saving many a shin from a coffee table or desk), and has led with an expansive array of attractive experiences to help with retention that have just about hit the level of fidelity so as to not offend the 4K/High-Hz visual snobs (myself included).

I use a gaming console as the comparative point for pricing because Meta has focused marketing on two major applications where they’ve (presumably) seen the biggest uptake - fitness and gaming. To this end, packaging the headset at release with a game (Asgard's Wrath 2) that has the potential to be up there with Beat Saber as a killer app was smart, but the fact that this title also has immense appeal for more “core” gaming fans by being perhaps the first manifestation of a deep RPG/open-world experience (not entirely unlike some of the most heralded games that were released this year) was very smart and positions the MQ3 to be technology that is less of an add-on than a gaming console of sorts in its own right (buckle up on this one - what is/is not a “gaming console” is going to start getting weird).

But, a killer app or two does not make for a particularly sticky platform. The true breakout of the MQ3 was that the launch aligned with some significant bridges to important content libraries - the new Steam Link App allows for users to tap into their Steam library of PC games (and therein, a deeper well of more “advanced” VR gaming experiences) yet retaining the wireless formfactor of the headset, while the recent adoption of Xbox Game Pass cloud streaming opens up a massive library of (non-VR) games to try in a virtual living room of sorts.

In short, Meta adopted an ecosystem approach to pull in just about every potential VR or gaming experience that could reasonably be pumped through their headset, and in doing so has attained what no other VR device in the past has: A deep content well.

Further, though it may sound strange to propose that the MQ3 was released at an “ideal time” when what many regard as the stylish elephant in the room, Apple, are on the cusp of their debut into the VR space (or “spatial computing” in the avant garde product marketing puffery Apple leans into)...it is truly just that. The competitive space for VR gaming devices is fairly stale at this point. The advancements in the MQ3 makes it hard for even Meta to justify their year-old premium Pro SKU and boasts technology that rivals more expensive options such as the Valve Index or HTC Pro, both being a few years dated themselves in terms of technology and (notably) requiring a physical connection to a PC (meaning the actual price and form factor burden is significantly higher). The more recently released Sony VR2 shares similar issues (and then some) - usage requires a Playstation 5 in addition to a price point that is similar to the standalone MQ3, and is largely locked within Sony’s content library which has been diminished by a lack of backwards compatibility.

A Snapshot of the Modern VR Space: Steam Hardware & Software Survey, August 2003

In other words, though I don’t think MQ3 will catapult VR into mainstream consumer adoption, it does have the potential to do so for gaming consumer adoption. This may seem like a booby prize for the VR-addled future technologist dream of, yet it is an important step - gaming is at the forefront of consumer technology adoption. As the gaming fans go, so too will mainstream consumers (eventually). The MQ3 has achieved something in the VR space that is noteworthy: It’s not just a good option for gaming enthusiasts who want to experience VR, it's conceivably the best option in the current market where gaming is the primary use case.

The gaming-centric value proposition of the MQ3 is a stark comparison to the impending offering from Cupertino in just a few months. Apple has all but stated that the Apple Vision Pro (AVP) is not a gaming device, but rather a spatial computing platform that augments the traditional computing experience (wonks will recognize I’m bleeding VR/MR/XR/etc. for the sake of simplicity, but for most consumers these specific applications aren’t as important relative to the more generalized category of “the giant piece of electronics that is strapped to my face”).

Detractors of the AVP have pointed to this semi-narrow framing and comparatively outrageous price point ($3500, or roughly more than the cost of a MQ3 [$500], Valve Index [$1000], HTC Vive [$1400], and Playstation VR2 [$550] combined), whereas proponents reference Apple’s uncanny ability to “create a market” for their devices given the success of the iPod, iPhone, and iPad (each massive disruptors for the MP3, phone, and tablet markets, respectively). This brings us back to the point above - if not gaming-focused VR, what market is the AVP set to disrupt in iDevice fashion?

The fallacy that APR optimist fall into is not recognizing that (however rudimentary) the markets that iDevices up-ended were already fairly well established, or at a minimum, the device(s) that the iDevice was designed to disrupt already had an established consumer use case. Switching to an iPod/iPhone/iPad wasn’t necessarily a difficult jump for consumers because they understood the intent and value of the device from predecessors in the market. VR as a technology category does not yet have that luxury. The value or problem being solved by VR isn’t quite as clear, and by divorcing from gaming the AVP is entering a space with no established market or precedent aside from replacing the everyday computer.

The AVP is in some ways attempting to climb the steep hill Meta has tried in the past by leading with its Horizon Worlds platform without much success in the past. Much time and energy has been spent trying to position VR as a substitute for our everyday reality, but missing that digital abstractions of everyday reality designed to appeal to a broader base of consumers forces us to focus on how much these experiences fail at the task: We all carry a compelling point of comparison (our own lived experiences in reality) and rendering some of our least compelling experiences in reality (a business meeting!) digitally doesn’t do much for us aside from making a bad reality worse.

In short: VR will continue to struggle simulating reality, when projecting a better fantasy is a far more attainable goal. You’ll see nary a mention of Horizon Worlds, the platform Meta is most incentivized for consumers to adopt, in the marketing for MQ3. The MQ3 is positioned as a machine that allows for a better fantasy rather than a worse reality. We have better substitutes for hanging out with friends or conducting a meeting than what VR can provide, less so for becoming a god guiding a roguish thief through ancient Egypt (ala Asgard’s Wrath 2).

The success of the AVP is predicated on being a breakout for replacing or augmenting (via MR) our experience of reality sufficiently enough to offset a market-bucking price point and the relative usability convenience of a laptop, desktop, or perhaps even just a smartphone. Comparatively, the MQ3 is a significant advancement in the VR space not because it has made any headway up this same steep hill, but because it has chosen a decidedly less steep hill to summit (gaming and fitness experiences).

Moreover, Meta has apparently learned what so many other new entrants from the broader technology must come around to - content is king. By allowing near-frictionless means of tapping popular content libraries, the utility of the Quest platform increases exponentially. Even if not a single gaming fan is lured into Horizon Worlds anytime soon, they’re significantly closer to doing so than they’ve ever been by adopting devices like the MQ3 for gaming. Meta prioritized a hill to climb (gaming VR adoption), and in doing so might finally be in a good position to take on the mountain (general consumer VR adoption). More generally, the market reaction to the Meta Quest 3 vs. the Apple Vision Pro will be an important bellwether for consumer adoption of VR, if not what consumers want or need from the technology moving forward.